A new reference margin option is being introduced to AgriStability. Starting with the 2025 program year, participants will be able to choose how they want their reference margin to be calculated – either as the optional reference margin or the accrual adjusted reference margin.

The optional reference margin (ORM) simplifies reporting for the reference period as accrual and inventory details are not required. The farm income reported for tax purposes, along with accrual, and inventory details for the program year are still required but only if the participant is in a claim position.

Participants have until April 30 to select the optional reference margin. As accrual adjusted reference margin (AARM) is the default method for the program, participants who do not select ORM will automatically have their reference margin calculated using the accrual adjusted reference margin.

Choosing your reference margin

Both the optional reference margin and the existing accrual adjusted reference margin have their advantages and participants will want to consider which best suits their farming operation.

The new optional reference margin reduces complexity for some participants, especially those who file their taxes on a cash basis, as the reference margin is calculated using the same method used for tax reporting.

On the other hand, the accrual adjusted reference margin considers inventory, payables, purchased inputs, and deferrals. It requires additional time and effort when first enrolling or returning to the program as more information for all reference years. However, the added information increases the precision of the reference margin calculation.

Comparing the reference margin options

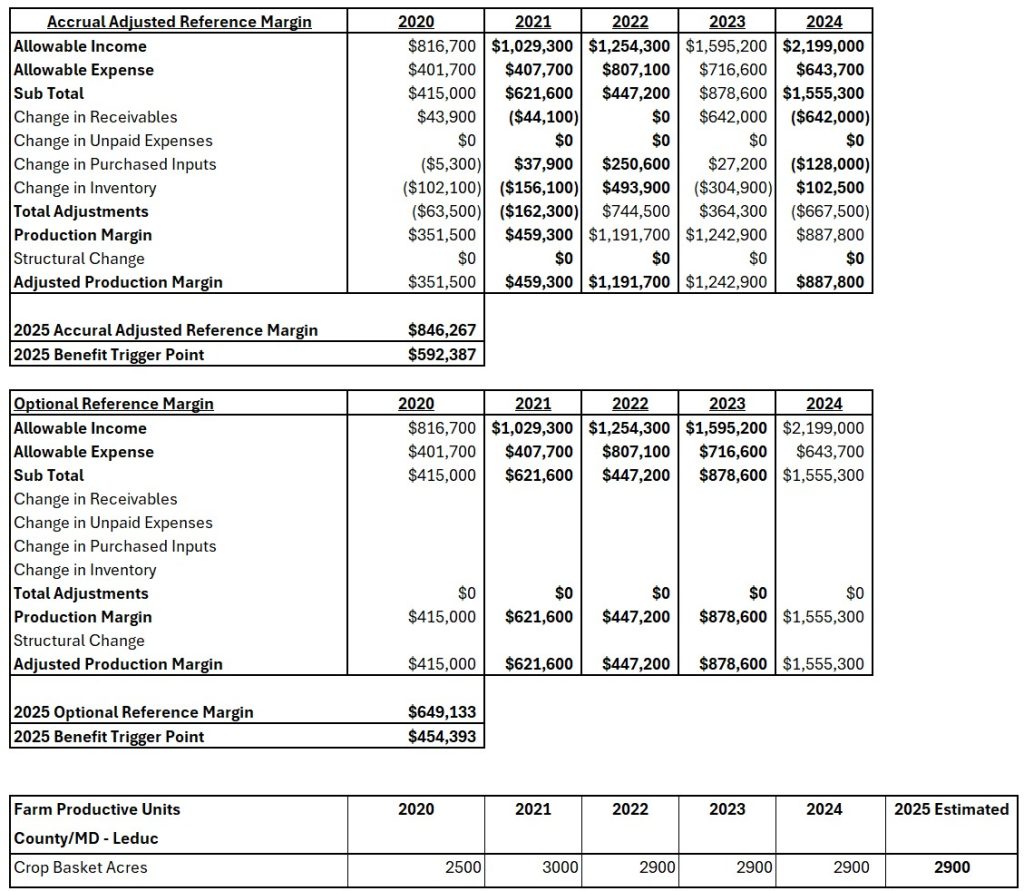

Example 1:

The first chart for example 1 illustrates the accrual adjusted reference margin calculation, while the second chart displays the optional reference margin. Due to consistent productive units on this theoretical farm, structural change is not implemented in these examples.

It is easy to assume that the options are similar because the reference margin is close to the same under each option, but a closer look at each year’s margins shows the differences.

- The Olympic average selected years have changed due to removing the impacts of the accrual adjustments.

- In the 2022 program year, there is a significant variance in the adjusted production margin when accruals are included compared to when they are excluded. The accrual adjusted production margin is at almost $1.2 million with the accruals and $447,000 without them.

- The impact of all accrual adjustments is clear in each of the five years, and any significant change to the numbers will not be captured in the ORM.

- The years selected to create the reference margin also change under the two different reference margin options. A careful consideration of each of the five last margins and accrual adjustments is critical to weighing the importance of including accrual adjustments in your reference margins calculation.

- Producers should also consider if the farm’s financial complexity is likely to change or if use of accruals is likely to increase, and what fluctuations might happen to the value of their inventory in coming years.

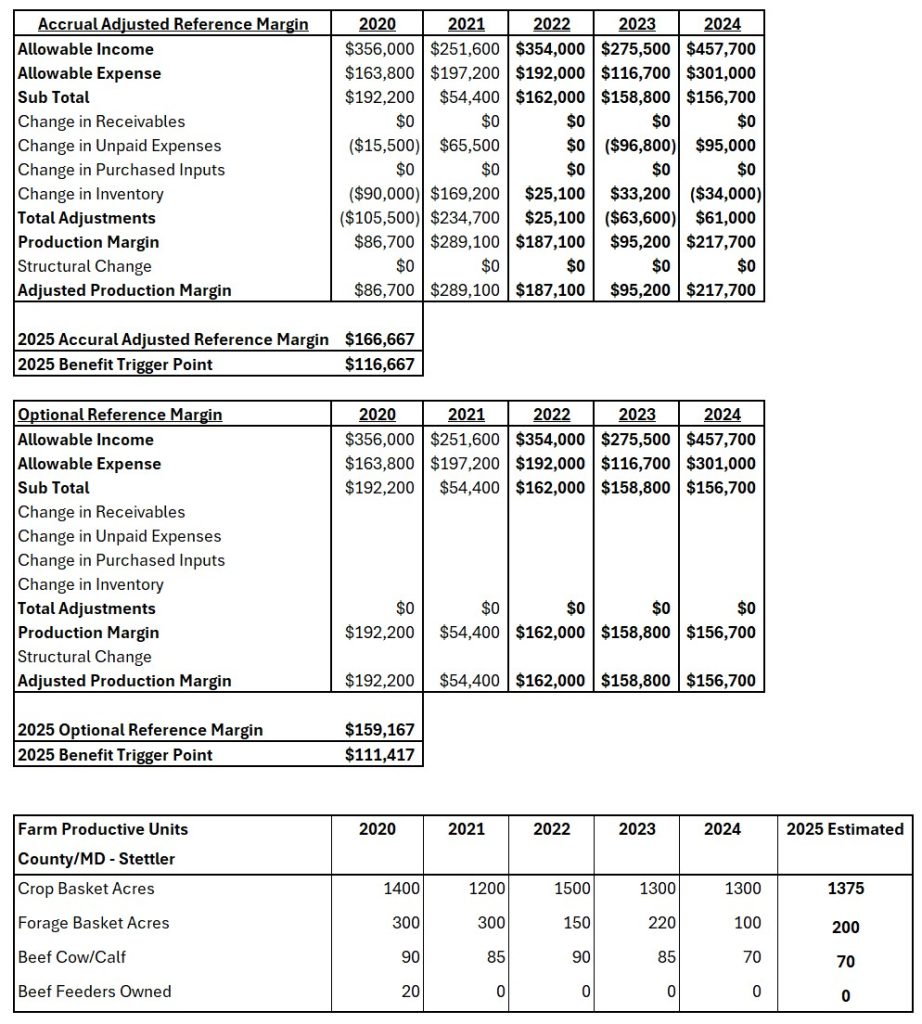

Example 2

The first chart for example 2 illustrates the accrual adjusted reference margin calculation, while the lower chart displays the optional reference margin. Due to productive units estimated for 2025, on this theoretical farm, structural change is not implemented in this example.

It is easy to assume that the options are similar because the reference margin is close to the same under each option, but a closer look at each year’s margins shows the differences.

- The Olympic average selected years have remained the same in both reference margin calculations.

- The impact of all accrual adjustments is most evident in the 2021 reference year, where it is the highest year when you consider accruals in the calculation and the lowest year when accruals are excluded.

- A careful consideration of each of the five last margins and accrual adjustments is critical to weighing the importance of including accrual adjustments in your reference margins calculation. Producers should also consider if the farm’s financial complexity is likely to change or if use of accruals is likely to increase, and what fluctuations might happen to the value of their inventory in coming years.

In these examples, there is no structural change being applied to these operations. It is important to understand the impact of changes in production units for your operation. Increases and decreases in production units may have an impact on your adjusted production margin in each year and the overall reference margin calculation.

A 2025 reference margin calculator is available in the Income Stabilization resource area; select AgriStability and Calculator in the filters to refine your results. Varying the production units in the calculator will demonstrate the impact of structural change on your reference margin.

Selecting your reference margin

Participants have until April 30 to select their preference reference margin calculation. This can be completed through AFSC Connect or using the 2025 Reference Margin Election Form available on AFSC.ca Participants who do not make a selection will automatically have their reference margin calculated using the accrual adjusted reference margin.

Participants will be able to switch reference margins in future years, provided they met certain criteria. For example, producers who have not participated in AgriStability for at least four years and who pick the optional reference margin can switch to the accrual adjusted method in any future program year. Existing participants can also select the optional reference margin; however, they must remain with the optional reference margin calculation for a minimum of four program years.

“Participants will want to take time to carefully consider which reporting option is right for their operation,” commented Daniel Graham, AFSC AgriStability and Pricing manager. “The accrual adjusted reference margin is more precise, but the optional reference margin is simpler and can give both new and returning participants a chance to see if AgriStability is a fit for their operation.”

Additional resources